The report

"Gesture Recognition & Touchless Sensing Market

by Technology (Touch-based & Touchless), Application (Consumer

Electronics, Automotive, & Others), Product (Biometric &

Sanitary Equipment) & by Geography - Global Forecast to 2020",

The gesture recognition & touchless sensing market is expected to

grow from USD 5.15 Billion in 2014 to USD 23.55 Billion by 2020, at a

CAGR of 28.2% between 2015 and 2020.

Browse 83 market data tables and 75 figures spread through 192 pages and in-depth TOC on “Gesture Recognition & Touchless Sensing Market - Global Forecast to 2020"

Some of the major companies in the gesture

recognition & touchless sensing market include Intel (U.S.),

Microsoft Corp. (U.S.), Cognitec Systems (Germany), GestureTek (U.S.),

CogniVue (Canada), eyeSight (Israel), PointGrab (Israel), SoftKinetic

(Belgium), PrimeSense (Israel), Cross Match Technologies, Inc. (U.S.),

Microchip Technology Inc. (U.S.), Qualcomm Inc. (U.S.) and so on.

The scope of the report covers detailed information

regarding the major factors influencing the growth of the gesture

recognition & touchless sensing market such as drivers, restraints,

challenges, and opportunities. A detailed analysis of the key players

has been done to provide insights into their business overview, products

and services, key strategies, new product launches, mergers &

acquisitions, partnerships, agreements, collaborations, and recent

developments associated with the gesture recognition & touchless

sensing market.

The entire gesture recognition market has witnessed

various advances after the launch of Microsoft Kinect which is meant for

gaming consoles of Xbox 360 launched by Microsoft (U.S.). After the

launch of Kinect, manufacturers and other players from the gesture

control industry value chain started focusing on consumer electronics

for gesture-enabled solutions. Currently, laptops, TVs, smartphones, and

so on with the gesture recognition technology are available in the

market. Similarly, touchless sensing products which primarily consist of

the touchless sanitary equipment and touchless biometrics are gaining

popularity. Currently, looking at the increasing rate of cybercrimes and

illegal trespassing, the biometric authentication market has gained

pace.

Growth in the E-Passport Program acts as a major driver for the market

With the introduction of biometrics and computer

chips, e-passport represents a major trend in the passport applications.

The face detection technology is used in e-passport, where a user’s

face is matched against the image held in the passport database; this

confirms that the person has not applied for a travel document in

another name.

To reduce the threat of identity fraud, governments

of various countries are implementing the e-passport program. The

International Civil Aviation Organization (ICAO), which sets the

principles and rules based on which international flights are conducted,

is also supporting the biometric technology to counter identity fraud.

The compulsory implementation of e-passports for the International Civil

Aviation Organization (ICAO) member countries by 2015 would boost the

market for the biometric technology.

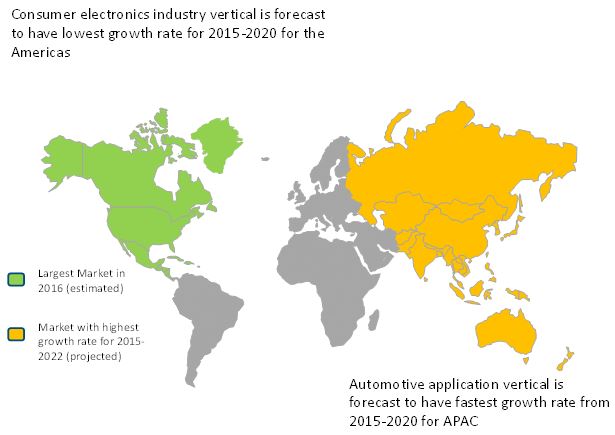

Consumer electronics vertical to play a key role in the gesture recognition market

The application in consumer electronics is likely to

hold a large share and lead the overall gesture recognition market

between 2015 and 2020 owing to the commercialization of the technology

in smartphones, tablets, smart TVs, set-top boxes, and gaming consoles.

There has been an increase in the production of gesture-based

interfaces, which enable users to control devices or software using

natural body movements and gestures. These interfaces are being

incorporated into a wide range of devices, including interactive digital

signs, medical equipment, arcade game machines, and robots among

others.

The application in the automotive sector to grow rapidly during the forecast period

In the automotive sector, gesture recognition is

under pilot testing with efforts concentrated towards integrating the

technology into in-car infotainment accessories. The endeavor would

enable a driver to control air-conditioner, music system, climate

control, and GPS along with other functionalities through gesture

recognition. It is meant to remove a driver’s distraction while changing

various modalities in a car. The technology provides a driver the

facility to operate these modalities simultaneously using simple hand

gestures which are possible with the help of IR and CMOS sensors and

cameras attached to infotainment devices. Infrared sensors are installed

near the gear lever to limit their functionality over a small area and

thus prevent accidental usage by other people in a car.

Automotive majors such as Hyundai (South Korea),

Mercedes Benz (Germany), Toyota (Japan), Honda (Japan), and BMW

(Germany) have come up with concept cars displaying integrated gesture

recognition capabilities.

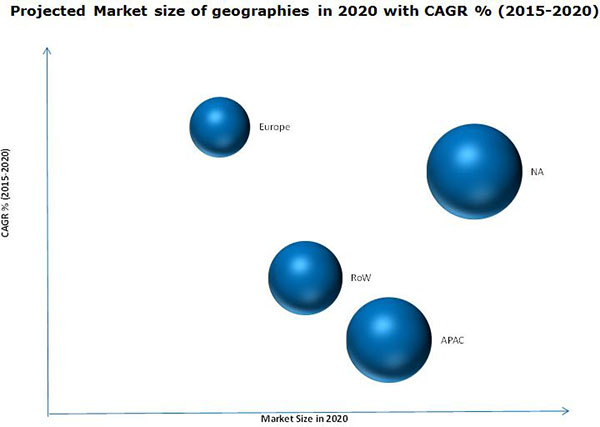

The Americas expected to hold the largest market share; APAC to grow at the highest rate

The Americas is expected to hold the largest market

share and dominate the gesture recognition & touchless sensing

market between 2015 and 2020. The increasing concerns towards national

security, especially after 9/11 terrorist attacks have significantly

driven the biometrics market in the U.S. The regulatory-driven

activities and initiatives taken by governments in the Americas have

enabled the large market size of the biometrics market in this region in

2012.

APAC is expected to rank first in the gesture

recognition market and third in the touchless sensing market during the

forecast period. The biometrics market in APAC is set to grow due to

technological advancements, increased awareness amongst masses, and

lowered costs. As organizations have become more security-conscious,

biometric solutions are expected to grow in terms of usage and

importance.