Lithium Ion Battery Market by Type (Li-NMC, LFP, LCO, LTO, LMO, NCA), power Capacity (0 to 3000mAh, 3000mAh to 10000mAh, 10000mAh to 60000mAh), Industry (Consumer Electronics, Automotive, Medical, Industrial), and Region - Global Forecast to 2025" The overall lithium ion battery market is expected to grow from USD 37.4 billion in 2018 to USD 98.0 billion by 2025, at a CAGR of 15% from 2018 to 2025.

• Download Informational PDF Brochure :- https://www.marketsandmarkets.com/pdfdownloadNew.asp?id=49714593

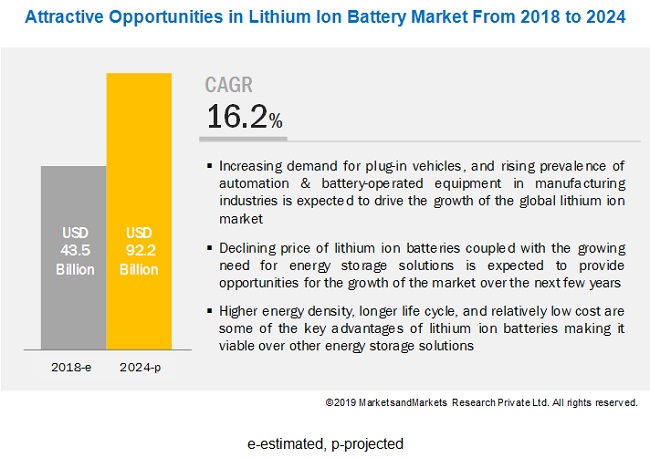

Need for high power and energy density has created demand for reliable and safe batteries for industries such as automotive and consumer electronics. Factors such as increasing demand for plug-in vehicles, growing need for automation and battery-operated material-handling equipment in industries, growing demand for smart devices and other industrial goods, and high requirement of lithium-ion batteries for various industrial applications are driving the growth of the lithium ion battery market.

Based on Type, Lithium Nickel Manganese Cobalt Battery to register fastest CAGR between 2018 and 2025

The market for lithium nickel manganese cobalt battery is expected to grow at the highest growth rate from 2018 to 2025. The energy density of NMC batteries is its primary strength. It achieves this energy density with good stability due to the use of an optimum ratio of nickel manganese and cobalt. It also has a good charge and discharge cycle. These features enable its application in industries such as automotive.

Power capacity range of 3,000–10,000 mAh is expected to grow at the highest CAGR during the forecast period

Lithium ion batteries with power capacity range of 3,000–10,000 mAh is expected to grow at the highest CAGR between 2018 and 2025. These batteries are often grouped together to form modules, and these modules are used in applications requiring heavy loads. Its heavy power capacity makes it useful for industries such as in electrical vehicles and industrial uses. Besides, the market for 0–3,000 mAh held the largest market, in terms of value, in 2018. This range is majorly used in consumer electronics industry. Around 90% of consumer applications have the power capacity in range of 0–3000 mAh.

Europe expected to be the fastest-growing market for Lithium-ion Battery during the forecast period

Europe is expected to be the fastest-growing market for lithium ion battery from 2018 to 2025. Europe is home to some of the largest battery manufacturers such as Saft (France) and FIAMM (Italy). The consumer electronics market for wearable devices is witnessing a positive growing curve in Europe. Presence and active association in Europe such as Association of European Automotive Industrial Battery Manufacturers and PRBA is supporting the use of lithium ion battery in different application in safe mode by their set standards and certification.

Key players operating in the lithium ion battery market include BYD Company (China), LG Chem (South Korea), Panasonic (Japan), Samsung SDI (South Korea), BAK Group (China), GS Yuasa (Japan), Hitachi (Japan), Johnson Controls (Ireland), Toshiba (Japan), Lithium Werks (The Netherlands), CALB (China), Saft Groupe, (France), VARTA Storage (Germany), Farasis Energy (California), and Sila Nanotechnologies (California).

About MarketsandMarkets™

MarketsandMarkets’s flagship competitive intelligence and market research platform, "Knowledgestore" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com