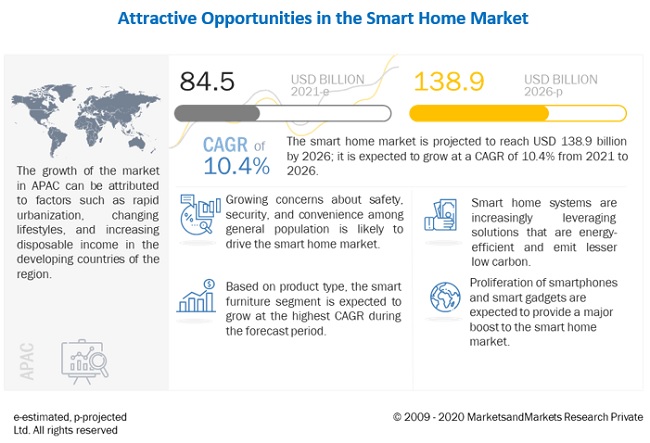

The smart home market in APAC is expected to grow at a

high rate between 2017 and 2023, owing to the rising number of new

residential projects and the increasing initiatives to strengthen the

building infrastructure in the region. The presence of a huge end-user

base in advanced economies such as Japan and South Korea and the growing

demand for energy management systems are also expected to fuel the

growth of the smart home market in this region.

• Download Informational PDF Brochure :- https://www.marketsandmarkets.com/pdfdownload.asp?id=121

• Download Informational PDF Brochure :- https://www.marketsandmarkets.com/pdfdownload.asp?id=121

The major companies operating in the smart home

market include Siemens AG (Germany), United Technologies Corporation

(US), General Electric Company (US), Schneider Electric (France),

Honeywell International, Inc. (US), Ingersoll-Rand PLC (Ireland),

Johnson Controls, Inc. (US), ABB Ltd. (Switzerland), Legrand S.A.

(France), Samsung Electronics Co., Ltd. (South Korea), Acuity Brands,

Inc. (US), Lutron Electronics Co. Inc. (US), and Leviton Manufacturing

Company, Inc. (US).

The market for smart homes was valued at USD 54.97

Billion in 2016 and is expected to grow at a CAGR of 13.61% between 2017

and 2023. The key drivers contributing to the growth of this market

include significant advancements in the IoT market; increasing need of

the consumer for convenience, safety, and security; and rising need for

energy saving and low carbon emission-oriented solutions.

The smart home market, on the basis of product, has

been segmented into lighting control, security & access control,

HVAC control, entertainment & other controls, home healthcare, smart

kitchen, and home appliances. Lighting control held the largest share

of the smart home in 2016. The growth of this market can be attributed

to the capability of lighting control to reduce electricity consumption

in homes as the sensors adjust the intensity of artificial light

according to the intensity of natural light. Entertainment has become an

important part of life as it provides relaxation and rejuvenation. The

most important feature of entertainment control is the ability to

integrate multi-room entertainment systems. The major controls used to

control and regulate the entertainment systems in smart homes are audio,

volume, and multimedia room controls.

The growth of the market for audio, volume, & multimedia room controls is driven by the convenience offered by these controls for managing as well controlling the entertainment systems within a house. The advancements in wireless communication technologies is a major factor boosting the growth of the market for home theater system controls, thereby driving the overall market for entertainment controls.

• Ask for Sample Pages of Report :- https://www.marketsandmarkets.com/requestsample.asp?id=121

The growth of the market for audio, volume, & multimedia room controls is driven by the convenience offered by these controls for managing as well controlling the entertainment systems within a house. The advancements in wireless communication technologies is a major factor boosting the growth of the market for home theater system controls, thereby driving the overall market for entertainment controls.

• Ask for Sample Pages of Report :- https://www.marketsandmarkets.com/requestsample.asp?id=121

North America held the largest share of the global

smart home market in 2016, owing to the factors such as increasing

demand for reliable home energy management systems, enhanced home

security levels, and growing popularity of integration of smart devices

such as tablets and smartphones in smart home solutions. The smart home

in Asia Pacific is expected to grow at the highest rate during the

forecast period. actors such as the strong economic growth, increasing

population and improving standards of living, and rapid urbanization

leading to a sophisticated infrastructure are driving the growth of the

market in this region.

South Korea held the largest size of the smart home in APAC in 2016. However, with the growth of the smart home industry and large-scale implementation of smart home system hardware and software solutions in China and Japan, the market in these countries is expected to grow at a higher rate than the market in South Korea during the forecast period. APAC is considered as a huge market for smart homes because of the considerable rate of implementation of various products such as lighting controls and HVAC controls in the region.

South Korea held the largest size of the smart home in APAC in 2016. However, with the growth of the smart home industry and large-scale implementation of smart home system hardware and software solutions in China and Japan, the market in these countries is expected to grow at a higher rate than the market in South Korea during the forecast period. APAC is considered as a huge market for smart homes because of the considerable rate of implementation of various products such as lighting controls and HVAC controls in the region.

Several smart home products have reached their maturity stage in certain regions. Most of the residents in regions such as Europe and North America have been using smart thermostats, smart meters, HVAC controls, and lighting controls for a long time. As the switching cost of these products is high, consumers do not replace them soon after installation. This acts as a restraint for the market growth.

This company is also focusing on strategic partnerships, collaborations, and product launches to grow in the market. It is also attempting to increase its sales and operations in developing economies such as China and India. Moreover, the company is concentrating on enhancing its product portfolio by actively engaging with customers to design and offer innovative products according to their requirements. All these efforts would help the company sustain its competitive position in the market in the near future