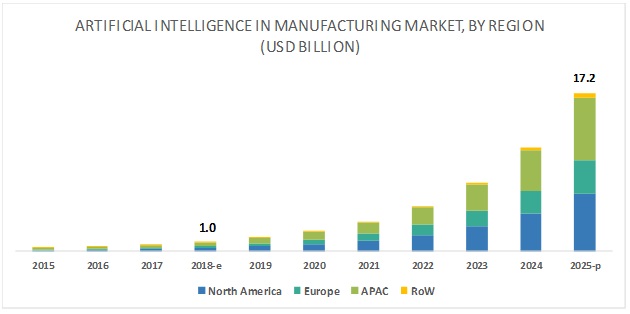

Artificial Intelligence in Manufacturing Market by Offering (Hardware, Software, and Services), Technology (Machine Learning, Computer Vision, Context-Aware Computing, and NLP), Application, Industry, and Geography - Global Forecast to 2025", the artificial intelligence in manufacturing market is estimated to be valued at USD 1.0 billion in 2018 and is expected to reach USD 17.2 billion by 2025, at a CAGR of 49.5% from 2018 to 2025. The market has huge potential across various industries such as automobile, energy and power, pharmaceuticals, and food and beverages. Increasingly large and complex data set available in the form of big data and evolving industrial IoT and automation drive the growth of this market. Improving computing power and declining cost of hardware are other key factors driving the AI in manufacturing market.

Browse 134 market data Tables and 48 Figures spread through 184 Pages and in-depth TOC on Artificial Intelligence in Manufacturing Market.

AI in manufacturing market for software to hold largest market during forecast period

The AI in manufacturing market for software segment is expected to hold the largest market from 2018 to 2023. A large number of companies such as IBM (US), Microsoft (US), SAP (Germany) and Siemens (Germany) are developing software solutions for various manufacturing applications; this is the key factor complementing the growth of software segment. Moreover, growing involvement of start-ups in the market is further complementing the growth of the software segment.

Computer vision technology to witness highest CAGR from 2018 to 2025

Computer vision technology is expected to foresee the highest CAGR throughout the forecast period. The growing adoption of computer vision in applications such as industrial robots, quality control, and material movement is propelling the growth of this technology in the AI in manufacturing market. Computer vision is mainly used for predictive maintenance and machinery inspection purpose. Companies such as Siemens (Germany) and Mitsubishi Electric (Japan) are using computer vision technology in their manufacturing plants.

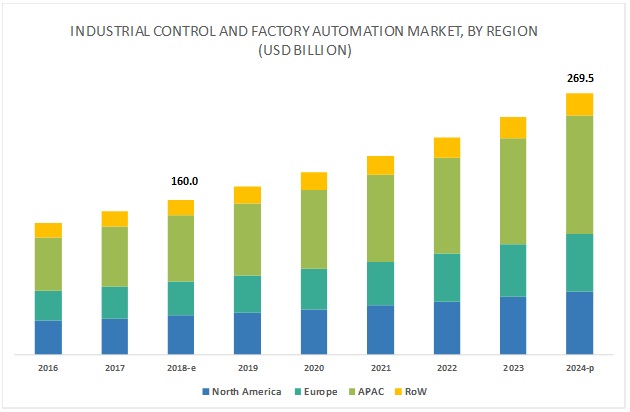

APAC leads AI in manufacturing market in terms of value

APAC to account for the largest size of the AI in manufacturing market throughout the forecast period. The presence of a large number of manufacturing companies in China and Japan along with the strong presence of automobile and electronics and semiconductor companies are driving the growth of the AI in manufacturing market in APAC. Moreover, the high adoption of industrial robots is expected to play a vital role in the growth of the said market in APAC.

The major companies profiled in this report are NVIDIA Corporation (US), IBM Corporation (US), Alphabet Inc. (Google) (US), Microsoft Corporation (US), Intel Corporation (US), Siemens AG (Germany), General Electric Company (US), General Vision Inc. (US), Data RPM (US) (now Progress Software Corporation), Clearpath Robotics Inc.(Canada), Mitsubishi Electric Corporation (Japan), Sight Machine (US), SAP SE (Germany), Oracle Corporation (US).

About MarketsandMarkets™

MarketsandMarkets’s flagship competitive intelligence and market research platform, "Knowledgestore" connects over 200,000 markets and entire value chains for deeper understanding of the unmet insights along with market sizing and forecasts of niche markets.

Contact:

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com

Mr. Shelly Singh

MarketsandMarkets™ INC.

630 Dundee Road

Suite 430

Northbrook, IL 60062

USA : 1-888-600-6441

newsletter@marketsandmarkets.com